Speaker: House prices and the "Magic Money"

162 Responses

First ←Older Page 1 … 3 4 5 6 7 Newer→ Last

-

James Butler, in reply to

I can see that constraining land supply will mean that rising demand will lead to rising prices. What I don’t see is where so much demand came from. If land supply were rising at the same pace as demand, then prices would remain stable.

Are we seriously suggesting that Auckland is meant to grow at roughly the rate that it’s property prices have been rising? So 26% in the last year alone? We’re meant to build a whole quarter of the city in one year?

No. Why would that follow? If the problem is that demand has exceeded supply - and that doesn't mean that there's suddenly more demand, just that the demand curve has crossed the supply curve - then you would expect prices to increase at a greater rate than before, as the value of the existing dwelling stock increases.

Also please let's talk about dwelling supply rather than land supply, it's less prone to being misinterpreted.

-

I think I've worked out what frustrates me most about this discussion. We're talking about the difference between housing value and housing debt, and trying to work out where the "extra" money is coming from; but I'm sure most of us have seen first-hand this missing money being created. Someone who bought a house in Auckland for $200k in 2005 now has a $700k asset, but no-one's lent them that money, and unless they sell then no offshore investor has swooped in to give it to them.

This is trivially obvious, which is I guess my point. We know that housing prices are rising dramatically, and we can argue all day about why that is (and I'm sticking with "Auckland's run out of all the easy places to add a dwelling" until I see good evidence that it's not the case); but the "magic money" gap only tells us that it has happened, and I can't see what it adds about why.

-

BenWilson, in reply to

No. Why would that follow?

I see what you mean, that you can't work out how much the demand curve moved from how much the price changed, without also knowing the shape of the demand curve and the supply curve, and how much the supply curve moved. And no one really knows the shape of these curves, because they are actually conceptually meant to apply to a single mass produced product. The closest we can get is grouping houses that are as similar as possible and keeping the history of the sale prices. Then we know where the curves crossed at various times. But that is all we know. We don't know the rest of the curves, because they are entirely hypothetical. They are not, and can't ever be data. So they are as useless as I thought. There was me hoping to find an actual use for them.

-

BenWilson, in reply to

We know that housing prices are rising dramatically, and we can argue all day about why that is (and I’m sticking with “Auckland’s run out of all the easy places to add a dwelling” until I see good evidence that it’s not the case);

I don’t think you’ll find such evidence, because, as you say price is a function of both supply and demand. So you can always blame both. I can’t even imagine what evidence there ever could be that would contradict “Auckland’s run out of all the easy places to add a dwelling”, without factoring in the demand side of the question. How many dwellings do we need? Until you can answer that, the statement is somewhat meaningless, and thus impossible to contradict. If we only need 1 new dwelling per century, then we’re far from having run out. If we need another hundred thousand houses per month, then yup, we’re out, and prices will skyrocket, but one could perhaps say that the need itself is the problem, not the number that we’re predictably failing to make.

Perhaps we could look at it another way: Maybe if instead of talking about how much supply we need for our demand, or how much demand we could curtail to fit with our supply, we talk instead about how fast we can accept prices increasing. Then we can aim to work on both of the factors to keep that growth to an acceptable range. I’d suggest that it should not be faster than wage and salary growth or the wealth gap can only widen.

Then we don’t have to have these futile discussions about which cause is most important. Instead we acknowledge that we should be both increasing supply and controlling demand, and then we do both at the same time. With variable levers so that we can get the balance right – some growth, but not too much growth.

Personally I think it should grow slower than wages and salaries to decrease the wealth gap.

The levers we can then tinker with are pretty clear. For supply, natural technological change is always a upwards driver, but it’s not controllable. Increasing the speed of approvals is a tap that can be turned up or down. For demand, interest rates are a lever we already use. Limits on foreign capital flows are another, and they could free up the other lever considerably. Trying to do it all with interest rates is like trying to swim with one arm. Then there’s the obvious possibility of redistribution through various subsidizations. I’m sure there’s others.

It’s so typical of economics as a discipline that we wouldn’t work out how much demand is a factor by deliberately controlling it the way we’d work out how something in the natural sciences works. Experimentation is virtually seen as an evil in economics. Which means that we really struggle to move beyond voodoo.

-

Russell Brown, in reply to

Personally I think it should grow slower than wages and salaries to decrease the wealth gap.

The levers we can then tinker with are pretty clear. For supply, natural technological change is always a upwards driver, but it’s not controllable. Increasing the speed of approvals is a tap that can be turned up or down. For demand, interest rates are a lever we already use. Limits on foreign capital flows are another, and they could free up the other lever considerably. Trying to do it all with interest rates is like trying to swim with one arm. Then there’s the obvious possibility of redistribution through various subsidizations. I’m sure there’s others.

Another obvious answer would be "whatever Germany does”. Which appears to revolve around strong tenancy rights and a culture of long-term rental. Although things may be changing a bit in Berlin.

-

Thing that has been bugging me about this discussion, which I think presents an alternate hypothesis for the magic money gap.

There seems to have been an underlying assumption by a lot of commenters that those buying houses have houses. Which is probably true, if you’re over a certain age, debt is needed by those buying a house worth more than the one they have.

But if we remember that debt is also needed by those that don’t have a house yet, then… The gap could be explained by the decreased debt load due to the decrease in new entrants into the market. That is, the “gap” is a reflection of the lockout of the younger population from the mental housing market.

What have I missed?

-

David Hood, in reply to

While there might be an element of that, the bit you've missed when you say " if you’re over a certain age, debt is needed by those buying a house worth more than the one they have." is it leads to the next link in the chain of "who you are selling your house to"- either you sell your house to someone (and at the end of the chain someone needs to load up on debt).

-

James Butler, in reply to

Then we don’t have to have these futile discussions about which cause is most important. Instead we acknowledge that we should be both increasing supply and controlling demand, and then we do both at the same time.

[...]

The levers we can then tinker with are pretty clear. For supply, natural technological change is always a upwards driver, but it’s not controllable. Increasing the speed of approvals is a tap that can be turned up or down. For demand, interest rates are a lever we already use. Limits on foreign capital flows are another, and they could free up the other lever considerably. Trying to do it all with interest rates is like trying to swim with one arm. Then there’s the obvious possibility of redistribution through various subsidizations. I’m sure there’s others.Minor quibbles with two of your levers. Restricting foreign investment is a tool you might consider using, but I suspect that if you can keep price growth down other ways then it simply won't be needed - why would anyone who doesn't want to live here want to invest in an asset whose value grows slower than wages? And subsidies have to be used very carefully - for example in the current situation, giving more money to buyers might help equalize the relative buying power of some groups but overall it would push prices up even faster.

-

This is probably the right place in the discussion to push LVT and UBI. Subsidise low income buyers, and penalise high-income rentiers.

-

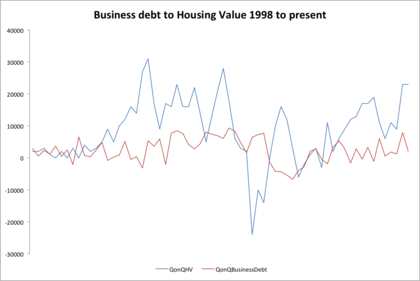

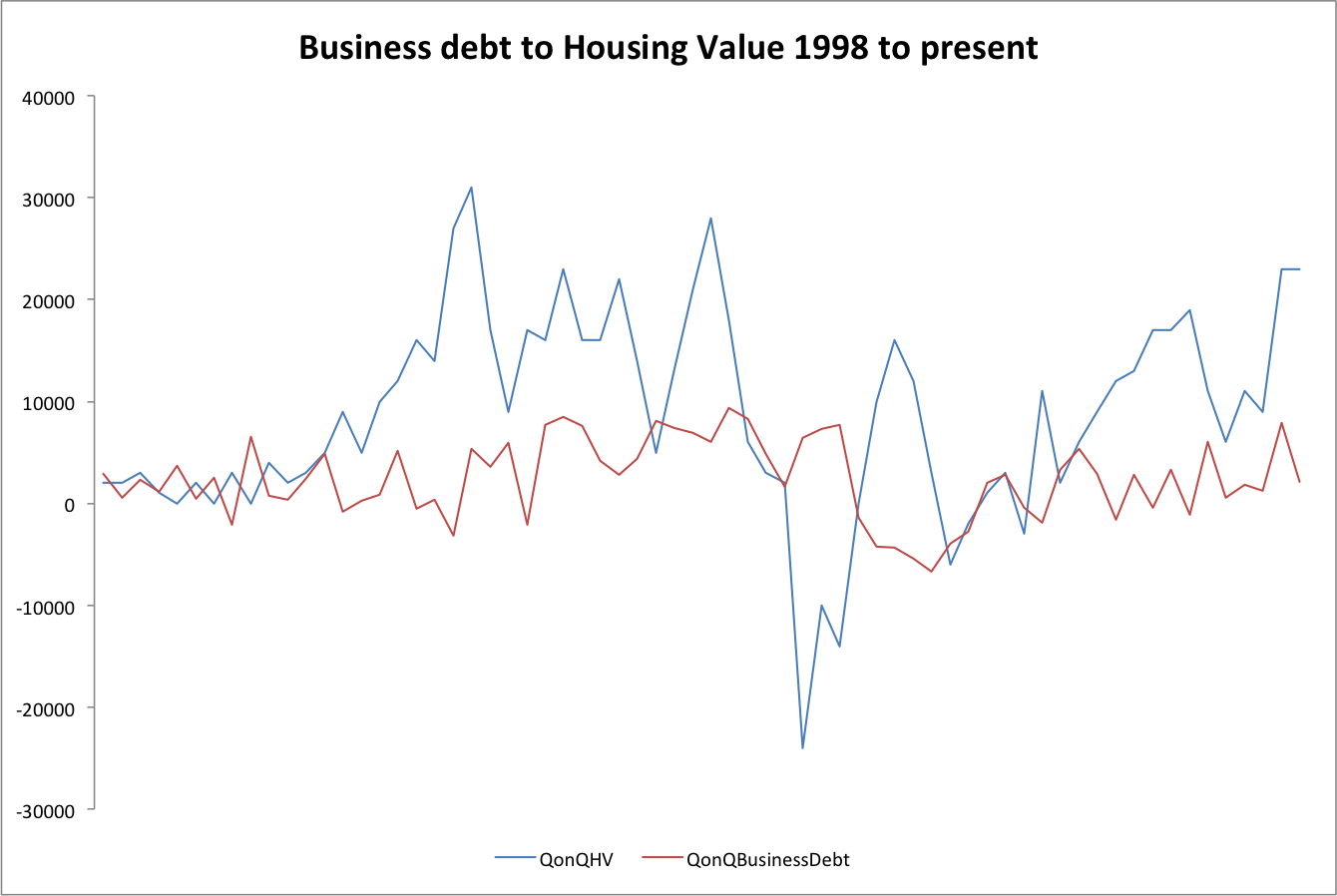

While it hasn't really come up in this forum, this is an example what I mean by "not detectable in other sectors of the economy"- this is business debt to banks, which if there was a growing relationship to house price would suggest some kind of mass commercial move in over the past 15 years. Now the data only goes back to 1998, but it looks like this graph.

For those interested in such things, that is an R squared relationship of 0.003, and no I did not misplace a decimal point. So that would have trouble having less of a relationship if business borrowing was actively avoiding the sector.

-

Greg Dawson, in reply to

is it leads to the next link in the chain of “who you are selling your house to"- either you sell your house to someone (and at the end of the chain someone needs to load up on debt).

But… What if there isn’t an end? As in, new entrants drop out of the market, crazy loon A and crazy loon B both have a moment and swap their $150k houses for $1.5m on paper. The new entrants would have to pay the crazy loon prices, but that might still result in a net drop in the total debt if the number of entrants has dropped steeply enough.

ETA: and the volume would stay high if the loon-swapping continued at a feverish pace, even while potential new entrants backed away slowly with fear in their eyes.

-

David Hood, in reply to

So are the two crazy loons "lending" each other the money for the transaction? I think that is verging towards real estate fraud cases you occasionally here about from overseas.

Under that scenario everyone else with a house would need to be not selling, as any non-loon sales at the then current price would be bringing the valuation figure back towards reality.

You also need the people excluded to be permanently out of the market, because if they do save up to the new (much higher) 25% deposit, they then take on much more debt when they actually enter, and that brings debt up to balance rather than prices down.

-

But I do agree that in a imaginary market where people only ever "buy" houses of the same value by swapping them in private sales with people of the same value houses for mutually agreed arbitrary amounts, then house value would be a meaningless measure.

I don't think we have any evidence that housing works that way though.

-

Greg Dawson, in reply to

Under that scenario everyone else with a house would need to be not selling, as any non-loon sales at the then current price would be bringing the valuation figure back towards reality.

You also need the people excluded to be permanently out of the market, because if they do save up to the new (much higher) 25% deposit, they then take on much more debt when they actually enter, and that brings debt up to balance rather than prices down.

That's exactly the scenario I'm proposing.

Collective lunacy grips the house buying and selling market, and those who already have houses trade for other houses (obviously not via direct swaps, but managed transitions via helpful banking institutions) at ever more loony paper values.

The ever-shrinking proportion of new entrants who manage to save 25% of the loon price-point load up on debt, but there are so few of them that the total value of debt as a proportion of total house value drops away from its prior level.

And yes, more and more people are permanently excluded from the market because the new loon-based entry point is insurmountably higher than their ability to hoard spare cash.

-

obviously not via direct swaps, but managed transitions via helpful banking institutions)

That just adds the debt as small amounts for lots of people rather than a lot for one person, as soon as you start involving third parties or shifting between value ranges. the debt still goes up.

Also the number of houses is increasing. Those houses must, by definition, break that chain of loons because it cannot be a "swap" (and as an aside, no the number of houses is not a good predictor of price either). Anytime anyone wants to exit the Nz house market (or does so involuntary) then that is not a swap either. So the network effect/ chain kicks in and those prices have to be justified by money.

-

Katharine Moody, in reply to

why would anyone who doesn’t want to live here want to invest in an asset whose value grows slower than wages?

To make use of it as a refuge in case of civil unrest in ones country-of-origin, or in case one falls foul of the authorities in ones country-of-origin.

-

Greg Dawson, in reply to

Thanks for explaining. Still think there is a factor down to the decreasing number of new entrants, but not the whole shebang.

It really would be good to have volume as well as value information. So much easier to try and figure things out if we could see variations in the unit value of loans too.

-

Katharine Moody, in reply to

why would anyone who doesn’t want to live here want to invest in an asset whose value grows slower than wages?

Then there is also the opportunity of rental returns growing at a rate higher than wage growth, regardless of underlying asset valuation. This is in part what happened in the US in the fallout of the sub-prime crisis;

Wall Street entities bought up hoards of foreclosed houses;

http://www.zerohedge.com/news/2015-07-26/these-13-us-cities-rents-are-skyrocketing

-

to some extent the fundamental difference between an internal market "tulip" boom and an external wave of capital is that in an internal boom someone inside the economy has to front up with the money at some point.

-

linger, in reply to

You also need the people excluded to be permanently out of the market

Not necessarily – people (in or out of the market) aren’t immortal. What you do need, though, is for the average lag time before people can enter the market to keep increasing over time.

-

David Hood, in reply to

true, for permanently I would have been better saying something like "for as long as you are measuring"

-

While I appreciate the value of testing David's analysis, especially given that some of the way money moves around in banks and in housing markets is somewhat arcane, I also find myself somewhat bemused by the discussions.

Yes it's possible David's analysis misses something.

But it is also pretty clear that David's analysis and the accompanying hypothesis is a very good fit for all the current observations.

Any hypothesis explaining rising house valuations needs to explain some of the other observations. And yes some of those data are not strong.

There is considerable reporting of Real estate activity offshore, very enthusiastic real estate activity all of which costs real estate companies money and that strongly suggests there is value in it for the real estate companies.

There is data suggesting a significant number of empty houses.

There is a complete lack of activity outside Auckland.

There appears to have been very little impact on prices from the construction of large apartment blocks.

And yes there is a lot of anecdotal reporting of houses being bought by offshore buyers.

All that together suggests that the market is not simply responding to a lack of supply but is instead responding to an increase in external buyers with external money.

What bemuses me is that people seem weirdly resistant to that idea. I honestly don't see anything surprising in the idea that offshore money would want to buy housing in New Zealand. As an explanation for the price rises it actually seems more logical to me than the constant insistence that supply is limited when it doesn't take much driving around Auckland to see huge new increases in supply.

-

Katharine Moody, in reply to

What bemuses me is that people seem weirdly resistant to that idea.

Yes, perplexing.

-

Lilith __, in reply to

All that together suggests that the market is not simply responding to a lack of supply but is instead responding to an increase in external buyers with external money.

What bemuses me is that people seem weirdly resistant to that idea. I honestly don’t see anything surprising in the idea that offshore money would want to buy housing in New Zealand. As an explanation for the price rises it actually seems more logical to me than the constant insistence that supply is limited when it doesn’t take much driving around Auckland to see huge new increases in supply.

What Bart said. Seems to me David's got strong evidence here. Is it being picked up by the media at all?

-

David Hood, in reply to

What bemuses me is that people seem weirdly resistant to that idea.

I would rate this an very receptive audience on this blog, not necessarily in full agreement (which is fine) but most people are willing to talk through the data (which I would call the true goal) rather than because of "appeal to authority" grounds. The medium (post plus comments naturally playing themselves out) may contribute to that as well as the audience.

Post your response…

This topic is closed.