Speaker: House prices and the "Magic Money"

162 Responses

First ←Older Page 1 2 3 4 5 … 7 Newer→ Last

-

Thanks so much for this, David. Will check it out much more thoroughly later today.

-

This is why I don’t think supply-side solutions are going to do much – the supply-side solutions are couched in terms of supplying the demand from local people, but we have no idea how big the supply would need to grow to deal with the demand from sources invisible to the New Zealand economy.

Totally agree. We also have no idea how this demand could change over time. It could treble over a year due to some policy change in any one of the very large countries in the world.

-

crap, looking at that graph I must have started this, I came back from my OE in 2004 and bought my house for cash, no mortgage …..

seriously though people moving to NZ with money is one cause of this, all in all that’s probably a good thing for the larger economy (wealth transfer inwards) though not so good for the Auckland housing market.

Just like looking at surnames it doesn’t prove directly that “people overseas are buying up our houses” more like that people with alternative sources of financing are buying our houses.

-

really like this post. i'm no big-city economist, but it seems pretty logical.

regarding where the money could be coming from: did you consider the two big changes in the mid-2000s, the Cullen Fund and Kiwisaver? Could property investment be being made from fund managers?

-

And just to prove how people outside of Auckland feel about all this angst about Auckland housing prices here's today's Tremain (ODT's editorial cartoon)

-

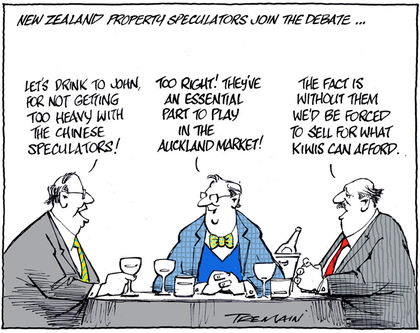

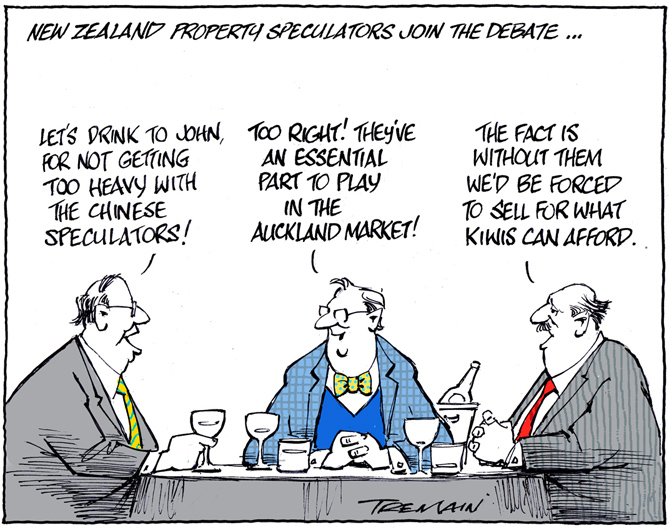

(and another view - Tremain from a few days ago)

-

Russell Brown, in reply to

This is why I don’t think supply-side solutions are going to do much – the supply-side solutions are couched in terms of supplying the demand from local people, but we have no idea how big the supply would need to grow to deal with the demand from sources invisible to the New Zealand economy.

Totally agree. We also have no idea how this demand could change over time. It could treble over a year due to some policy change in any one of the very large countries in the world.

Yes, this occurred to me after David posted the first of this stuff in comments on earlier posts: what nature of demand are we even planning for?

-

Authority X said it was supply constriction due to RMA restriction. I am sure they did.

It's surprising how often this is offered as a received truth.

-

Sacha, in reply to

Could property investment be being made from fund managers?

I sure hope not, if a correction happens.

-

David Hood, in reply to

crap, looking at that graph I must have started this, I came back from my OE in 2004 and bought my house for cash, no mortgage …..

seriously though people moving to NZ with money is one cause of this, all in all that’s probably a good thing for the larger economy (wealth transfer inwards) though not so good for the Auckland housing market.

You might individually have been part of that, but the actual immigration numbers are not a match to house price rises- I can go through much the same process showing a lack of relationship between arrivals and house value. So we get to the situation of access to capital (not identifiable within the New Zealand Economy) rather than people.

-

Paul Campbell, in reply to

You might individually have been part of that, but the actual immigration numbers are not a match to house price rises- I can go through much the same process showing a lack of relationship between arrivals and house value.

I think more you should take out the portion attributable to mortgages, then do something similar for immigration (do people like me coming back from OE even show up on anyone's radar?) and then look at the remainder

So we get to the situation of access to capital (not identifiable within the New Zealand Economy) rather than people.

which was sort of my point

-

David Hood, in reply to

Could property investment be being made from fund managers?

Perhaps individually, buying an investment property with their management fees, but there is no direct sign of Kiwisaver funds investing in residential property.

-

David Hood, in reply to

I think more you should take out the portion attributable to mortgages, then do something similar for immigration (do people like me coming back from OE even show up on anyone’s radar?) and then look at the remainder

Let's describe immigration and local borrowing as both fairly flat through to 2010.

-

David Hood, in reply to

what nature of demand are we even planning for?

I don't know what figure the government uses . Based on the past 15 years, a figure of demographic demand from local population + 60% would seem to be an optimal spot (I don't for a moment beleive this is the target figure) but in reality it is somewhere between 0 and 4 billion extra houses needed to stablise demand. And because of the unknowns that is a pretty wide error range.

-

David Hood, in reply to

i’m no big-city economist

that's OK neither am I (data handling I know). But it occurred to me that this is where there is supposed to be a relationship and the numbers stopped adding up. I'll describe it as Cuckoo's Egg situation of a discrepancy in the numbers.

-

the initial launch point (third quarter 2001) precedes the RMA

The RMA was enacted in 1991 and a Town and Country Planning Act preceded it (1977). I don't think there's been a free-for-all in land development in NZ (or in most developed countries) for a long time.

-

David Hood, in reply to

Well spotted, opps. I was think of the LGA (local government act) 2002., which free market types blame for red tape making house prices rise (without debt increasing at the same rate, through the power of time travelling back).

-

Greg Dawson, in reply to

but in reality it is somewhere between 0 and 4 billion extra houses needed to stablise demand. And because of the unknowns that is a pretty wide error range.

So… we can build 4 billion houses in Epsom, right? They just need to be... (grabs fag packet) ... twenty four thousand stories high. Too late to adjust the auckland plan?

-

David Hood, in reply to

twenty four thousand stories high

It would give Epson a special character.

-

BenWilson, in reply to

in reality it is somewhere between 0 and 4 billion extra houses needed to stablise demand. And because of the unknowns that is a pretty wide error range.

Yes, and hardly filling me with cozy feelings of security about the future stability of prices. If as few as 1 million people with a lot of money decided to make a beeline for NZ, locals would be drowned in capital and the class divide would turn into a bottomless chasm. Those already in property would make a killing. Those not in it would never get in, ever, unless they became independently very wealthy. Probably through inheriting property.

As someone in property (and likely to inherit more), I’m “safe”. As someone who wants this country not to degenerate into third world levels of inequality, I’m really concerned. At a global level, it’s this wonderful self balancing system. At a local level, entire countries could be completely ruined. Do we want to be that country?

I pick the number 1 million from thin air. It’s one four thousandth of the 4 billion upper limit you give. It’s one fifteen hundredth of the number of people in China. It’s one three hundredth of the number of people in the USA. Without any way of knowing the actual numbers, it’s picked as “very small compared to what it could be”. Maybe it’s conservative. Maybe it’s overestimating. Point is: Who knows? Shouldn’t we know?

-

Who benefits?

Why are the government(s) willing to allow those who benefit to continue to benefit?

Who is harmed?

Why are the government(s) willing to allow those who are harmed to continue to be harmed?

-

Greg Akehurst, in reply to

Russell, in much the same way that the Bush administration used the 9/11 tragedy to launch an attack on Iraq (a totally unrelated party - but you know, they all look the same, right??), the National Government is using the real hurt the Auckland housing bubble is causing to attack another piece of lefty socialist legislation (the RMA) that is inhibiting the rape and pillage plans of their key supporters.

-

Just trying to understand this:

If you had a country where house sales were very unusual (as was re-mortgaging to extract equity), but prices as indicated by the small number of sales were rising fast, then you'd get a corresponding rise in the value of the housing stock without a significant rise in debt?

Could it be that since 2008, most Aucklanders have been sitting on their gains and hence the house price value is increasing without a corresponding change in debt?

-

David Hood, in reply to

Well spotted, opps.

I updated the github version to

Authority X said it was supply constriction due to RMA restriction. I am sure they did. The RMA came in in 1991 (thanks to Rich of Observations for a correction here) and the LGA (the other main target) came in in 2002 and was implemented in 2003. Either requires a dose of time travel, but neither explain the lack of debt rise. We come back to if around 300 billion in the 800 billion in Housing Value gains is not explanable by inside the economy debt, how many houses do you need to build to satisfy that unknown demand- it has nothing to do with people, actual immigration is not a very good predictor of house prices.

-

David Hood, in reply to

If you had a country where house sales were very unusual

It might be possible to contract a sufficiently unusual situation to explain it, but it is very hard for those explanations to to leave traces in other parts of the economy- sudden simultaneous remortgaging should affect household debt (since prices are going up). A drying up of property so a smaller sample making the values less meaningful should show up as dramatic changes in sales numbers.

It could all by caused by the unusual market situation of one house that is being sold between people with overseas capital every month doubling each time. And that one house is now worth 256 billion dollars. But that would also leave secondary evidence.

Post your response…

This topic is closed.