Hard News: How the years flew by ...

101 Responses

First ←Older Page 1 2 3 4 5 Newer→ Last

-

Martin Brown, in reply to

Don't banks protect share borrowing via margin calls?

-

Stephen Judd, in reply to

Don't banks protect share borrowing via margin calls?

Yes. The thing is that shares are generally easily liquidated the same day (at least the ones you can buy on margin). And when I checked last, you usually couldn't go buy than 60% of a margin.

So yes, you definitely can borrow to invest in shares, you can do it through your broker by setting up a margin account, and actually it might make sense to buy an exchange traded fund or basket of blue chip shares using your revolving credit mortgage.... but the risks for you and the bank are rather different than with houses.

-

Russell Brown, in reply to

Baby boomers planning on moving to a retirement property out of Auckland, for instance, are advantaged by Auckland prices being as high as possible.

This might be me in, say, seven years' time. But I'm happy to argue against my own interest in this case.

-

Nowadays though I guess we have to think from the goveernments point of view. Having neglected to do anything about the housing ponzi/bubble, they have got a tiger by the tail. Everyone knows what is required. A ban on foreign buyers of existingg homes, a CGT, a government led crash building program and a way to rapidly free up land for intensification. But doing anything concrete that leads to a substantial (25%+) downwards price correction would completely tank that section of the Auckland economy that complains the loudest, destroy the wealth a significant porportion of the Auckland (and therefore NZ) middle class with all the knock on effects of that (here in my town in Spain unemployment has sat at 40% since the 2008 crash, anything approaching that level would probably lead to a complete breakdown of civic order in NZ) and could even seriously damage the banking system. So the government wants to stop runaway housing inflation, but is terrrified of the consequences if it does. So it is all jaw jaw in the frantic hope that might do something.

In the end, probably the only economically sane solution is policies designed to halt the upward price spiral without an actual downward correction, and some mild inflation combined with a wages policy that encourages actual wage growth. Unfortunately, the political establishment is completely enslaved by the magical thinking of neoliberalism, so intervention to build houses and encourage wage growth is an anathema, and the reserve bank act has removed from the policy toolbox the possibility of mild inflation to eat away at house prices.

So we are fucked, because the government won't do anything until the political cost of doing nothing is higher than the political cost of doing something, by which time the subsequent crash will be a economic disaster.

-

Kumara Republic, in reply to

So we are fucked, because the government won't do anything until the political cost of doing nothing is higher than the political cost of doing something, by which time the subsequent crash will be a economic disaster.

It seems the housing bubble is an ongoing game of chicken. Whoever's in charge if/when the bubble bursts will probably find themselves out of power for a generation in the same vein as Herbert Hoover and Forbes-Coates. The same goes if whoever's in power deliberately pushes the fiscal nuke button, and is seen to be the second coming of Joe Stalin.

I suspect that in private, Key & Little are both hoping that it's the other one who's holding the housing crash bomb if/when it goes off.

-

Tom Semmens, in reply to

I don´t think the country can afford to let the bubble burst.An economic disaster like the one in Spain just cannot be allowed to happen. We would have a civil war.

The only option is to stop prices rising and then let 10-20 years of inflation and wage growth to chip away at the affordability issue.

In the meantime, an entire generation will miss out on home ownership in Auckland. For them, we need reform to give tennants greater rights of tenure, government building programs for affordable apartments and terraced housing in cities with low entry level costs for those wanting to rent to buy or long term lease, and a recognition that this can never be allowed to happen again.

-

Ian Pattison, in reply to

counted as inflation, that woul

Either we blame the people who did the thing, or blame the system (or part of the system) they operate in. If you don't want to blame the people, the system needs fixing.

To my mind, this is just another example of how deregulation and neo-liberal economics have ruined the west.

-

Zach Bagnall, in reply to

The only option is to stop prices rising and then let 10-20 years of inflation and wage growth to chip away at the affordability issue.

That seems like the way to go. Auckland prices could fall 50% and still be considered "unaffordable". There hasn't been a fall like that since the 70s and it wouldn't be allowed to happen now, so I'm not even holding my breath for a correction let alone a full blown crash.

I'd like to see more incentives for investment outside of Auckland, and some effort to tilt investors away from property and back to productive economic activity.

Bart is right that NZ is relatively poor, but selling houses to each other (including to wealthy overseas actors) isn't helping that.

-

I'm on the cusp of moving back to New Zealand after 8 years living overseas. Unfortunately for me with my new job that means Auckland. There are certainly advantages, it will make life easier for my foreign fiance, being what passes for a big city in NZ and we have mutual friends there. The reasons for taking a job back in NZ are many and numerous but that is all by the by. At the end of the day no one is forcing me to accept Auckland as base (I was given other options but had to weigh other factors against those, one of which could have been Christchurch).

But I look at Auckland with a great measure of perplexity. In the 8 years I've been coming back as a tourist I've seen Auckland ebb and flow through a lens coloured by childhood memories of visiting grandparents and the fact my visits were fleeting days twice a year or so. Having spent the last year in France it was the last trip that made me really question it's growing absurdity. I took the SkyBus from the Airport to Downtown to run errands and that gave me a greater ability to observe Dominion Road with a critical eye. It is a major arterial road and yet there are so many large lots with small to average houses and certainly nothing flash. It seems to me that intensification here would also serve to provide the patronage for useful public transport on the corridor between the city and airport. I don't believe that intensification on such an arterial would materially affect amenity of the likes of Sandringham etc.

Of course, as all of you who live in Auckland know there are numerous examples like this across Auckland. Sprawling out makes very little sense to me.

I don't think we'll look to buy in Auckland. We're accustomed to living in small apartments, sans children for now. But I definitely feel the market is overheated and I worry about my friends exposure even though they have higher salaries than I will be starting on.

As a rental property investor (outside of Auckland) I actually think a CGT makes sense. But there are a range of actions the government needs to take and I don't see them realistically doing much save for maybe the housing tax, encouraging urban sprawl and more roads, glorious roads!

-

Isn't there already a CGT on homes other than the one you're occupying?

Edit: Holy shit, I guess not - except for the recent 2-year thing. That explains a lot.. -

Smoke and mirrors…?

CGT

I still can’t see that without thinking ’Computer Generated Tax’.

Therefore ‘SFX’ would be ’Special For-Ex’ - Mr Key’s speciality…I did see a nice new BMW the other day with the numberplate ‘GFC…’

how they must laugh, those Big-money Johnnies… -

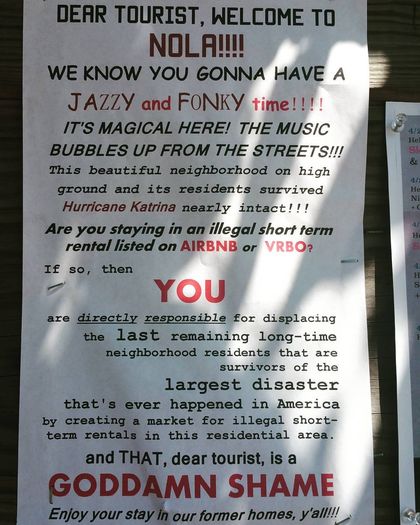

Reposting a pic placed by Dan Salmon in regard to deregulation, on the Uber thread.

I'm just wondering how many Air BnBs (and similar) are listed in Auckland these days - each one of those (or many at least) takes a family footprint out of the housing equation - apparently they are contributing to the killing of cities like New Orleans, Venice, Barcelona, Paris etc as far as local occupation goes...

-

Kurt Mastrovich, in reply to

A fairly significant amount. I also read an interesting article the other day along those lines. We just happened to be staying a couple of nights in an Airbnb apartment in Bordeaux and it really struck a chord. That said we were clearly part of the problem.

-

Housing affordability in Auckland and right across the market is more affordable now than when National came to power....

according to Nick Smith...

http://www.radionz.co.nz/audio/player/201798817

So be of good cheer folks...we're not fucked after all....

-

Lucy Telfar Barnard, in reply to

I heard that too, and snorted.

I have no idea whether the ratio of mortgage payments to incomes is higher now than it was when National got in, but even if it is (which I doubt), that's hardly the only indicator of affordability.

- The deposit required, as a percentage of income, must certainly be higher.

- Even though the interest rates are lower now than they were then, people can't make borrowing decisions based solely on what interest rates are right now, when mortgage rates can change. We need to have a buffer so that we're confident we can afford to pay the mortgage if interest rates increase.Nick Smith was correct when he said that some option wasn't "a silver bullet". There is no silver bullet. We need a whole range of measures, that collectively add up to action on housing affordability.

Banning overseas ownership would be a good start. Yes of course there will be workarounds, and we'll need to identify those and move to close those down too. It may be hard, but other countries manage to do it.

-

Paul Campbell, in reply to

Another factor is that the children of Boomers are quite happy for it to perpetuate because who do you think benefits when their parents eventually pop their clogs?

Our kids have been tolds not to depend on it in their live's plans, we're planning on spending it all, anything that's left when we go will be gravy

-

Rich of Observationz, in reply to

Doesn't a conventional hotel or backpackers (or indeed a supermarket, factory or sports arena) do exactly the same thing, in taking up acreage that isn't available for housing 'locals'?

(and at the margin, there is transfer between hotel and apartment block use - the Formule 1 on Wyndham St used to be a block of tiny apartments, for instance).

-

Ian Dalziel, in reply to

A fairly significant amount. I also read an interesting article the other day along those lines.

http://www.citylab.com/housing/2015/12/barcelona-airbnb-tourism/421788/

http://www.reuters.com/article/us-spain-tourism-airbnb-idUSKCN0QV1LR20150826

I noticed the problem too, when in an Air BnB in Venice (right by the Biennale sites in 'old Venice') - tricky rubbish collection schedules in a town with no trucks was creating a flashpoint between the original inhabitants and us 'transients' - and in Barcelona there was at least one Air BnB on each floor of the old inner city apartments we stayed in, ditto in Rome - something is gonna have to give, but it may already be too late...

-

Some products have more regulation than others. Alcohol has more rules for supply and purchase than milk or butter.

The rules around renting out housing seem to be based on an historic NZ model where renting was for students and young people in the few years between leaving school and buying your own house.

That a landlord can ask you to move out with 45 days notice when your kids are at the local school, playing local sport seems a bit harsh. That may be o.k. where most renters are transient students but these days that is no longer the case.

If you are a landlord, you are renting out housing; warm safe shelter is a human right. Renting housing is different from renting out diggers or wedding marquees. It should be subject to more regulation. Why don’t we have rent control, w.o.f. for housing, security of tenure?

A lot of the housing bubble is caused by people buying investment property. The investment is the primary concern, and becoming a landlord is secondary or not thought of at all and contracted out to a property manager.

If we are going to have a more renting culture, we should have good regulation to support this. As a side effect, if regulation forces landlords to be serious housing providers, the more causal property investors may start leaving the market.

-

Lucy Telfar Barnard, in reply to

Yes of course. But just because other things also decrease the availability of housing available to locals doesn’t mean that AirBnB isn’t a problem.

City/regional planners, in considering zoning, or applications to construct hotels/backpackers/supermarkets/sports arenas, consider the allocation of land to different purposes. Those purposes include farming, industrial and commercial manufacture, retail, sports facilities, housing tourists/short-term visitors, and housing residents in different intensities of housing.

When people rent their properties and spare rooms using AirBnB rather than renting or selling to longer-term residents, they change the ratio between housing available to short-term visitors, and housing available to long-term residents. But they don’t have to apply to the council to do so. So the planner’s ability to maintain the necessary balance in land allocation is compromised, and it is the long-term residents who suffer for it.

In the long-term, it may balance out. Hotels who lose custom to AirBnB may close and be converted to resident housing. But that’s not much comfort in the short term to the residents who can no longer find anywhere to rent because property owners have realised they can make the same profit by letting to short-term visitors instead.

-

Bart Janssen, in reply to

we’re planning on spending it all

I'd start to worry that they plan on cashing in early when they start gifting you Mt Everest expedition and base jumping holidays.

-

Golly.

This is a world wide problem. Most western world major cities are in the same boat.

There are multiple causes and solutions, and many mentioned here. My favourite solution is a decent social housing program with secure long term tenancy. And regional development (I am *never* going back to Auckland where I grew up, the quality of life is so much better in other parts of the country. Way way better. Off the chart better...)

But a cause that we are forgetting is the crash, throughout the stable section of the western world, of interest rates. Not so much that borrowing is cheap but that there are very few places to put capital for a decent risk adjusted return .

It will be interesting to see how much investment is from non-resident foreigners, we need many data to know and we have close to none (Chinese sounding names is racist cant - shame). That is probably "hot money", volatile. There is a good chance the "hot money" buyers will get spooked, liquidate and leave for any number of reasons.

Then as Paul Campbell pointed out a sudden increase of interest rates would wipe out a lot of investors and banks would be forced to liquidate.

Which ever way you look at it it is reasonable to expect that we will see a crash in the housing market, world wide. No government policy changes can prevent it or protect us (except decent secure social housing - but that is a communist plot apparently).

We are at an economic cross roads. All the old assumptions about wealth are getting turned on their head. Now the most valuable thing is ideas not factories, the value of labour is in free fall. This is a symptom, and expect some very rough weather ahead.

-

Ian Dalziel, in reply to

In the long-term, it may balance out. Hotels who lose custom to AirBnB may close and be converted to resident housing.

I think that's sort of what's going to happen in Chchch: the first flush developers will take a bath on their empty office buildings, and they'll be sold in fire-sales and get converted into apartment buildings (or mixed use as happens in other countries) - despite not being designed originally for such use.

-

OK, so if there is no political will to fix the bubble, what would a post burst plan look like? House prices plunge 50%-80%, mortgagee sales, government bail-out of the NZ branches of the Aussie banks (under pressure from over the Tasman), or bail-in using NZ bank accounts to buy bank shares? Would the government call a snap election so the public can compare the pain of the opposition's solutions to its own?

-

Rich of Observationz, in reply to

My current office building has an apartment hotel on the top floor.

Traditionally, a big difference between offices and residential was the former having a much higher stud to make room for services in the floor/ceiling, but with WiFi, that becomes less important.

Post your response…

This topic is closed.