OnPoint: Budget 2013: Bringing Down the House (Prices), but not really

89 Responses

First ←Older Page 1 2 3 4 Newer→ Last

-

Ian Dalziel, in reply to

Serco Server Farms?

We are quite literally worth more dead than alive…

Oh, I think the Powers-that-be might have Private Prisons, ready to use you as cheap labour for a while, first...

-

Wow is the IRD + Treasury really costing us over 10 billion per year?

-

Sacha, in reply to

I want to know how brokers could possibly 'earn' $50-100m for selling off an electricity company?

-

"chris", in reply to

Oh, I think the Powers-that-be might have Private Prisons, ready to use you as cheap labour for a while, first…

Isn’t that basically the jist of the budget? Sure they’d have to accommodate me for more than a decade before I show any profit, but you know, compared to the uncertainty of arrest and potentially losing one’s foreign job, home, friends and possessions, as the lesser of two evils I’d welcome that; 3 meals a day, a roof over my head and the certainty of a job, that sounds better than the freedom I new in New Zealand post graduation, truth be told, speaking only as one of the humanities of course. At least it’d be stable employment. I wish I were joking, but that makes a lot of sense given the options, at least more so than fixed repayment that I can’t meet and arrest for not doing so.

This so-called ‘good policy’ doesn’t really make one iota of difference to those who can’t afford the obligatory payments, To those who can, well perhaps the hideous stick truly and deeply is good policy, perhaps it’ll scare the bejeezers into Chuck defaulter, and if we’re seriously going take the leap and begin paying off the debt, hecksaw, why not do so in environs where its no longer incurring interest. I hear a decent proportion of 100,000 overseas borrowers returning could just do absolute miracles for the NZ job market. Sense by the truckload there. It's probably best to just come home now before the border arrest policy is implemented, before the influx at the. Or perhaps in some parallel universe people do in fact get into the situation where interest stacks up to the point where it becomes impossible for graduates to move back , that universe where New Zealand isn't a welfare state, and this policy will change all that at the speed of apathy.

At some point 6.2% unemployment, $1.7b jobseeker support and emergency benefit and $411.5m overdue student debt should meet up for a drink, who knows, they might even come to an understanding that old 441.5 is actually real good value.

-

Chris Waugh, in reply to

What you left out of that equation, "chris", is just how easy it is to set us overseas borrowers up as a target, especially media so readily accepts whichever narrative the authorities, political, bureaucratic or economic, put forward. And especially because we're overseas. We must be living the high life jet-setting around the place or something.

But what worries me about this border arrest thing is: arrest for what? The only specific thing I've seen mentioned, apart from "the worst of the defaulters" (define "worst"!) is unpaid child support. But really, what crime have these "worst of the defaulters" committed? Can people in New Zealand be arrested if they default on their mortgage or some other kind of loan? Or is missing a student loan repayment now some kind of tax evasion? Heh, if it is, it may well be worth talking to a lawyer. You know how jealously China guards its sovereignty - how would they react to the allegation that NZ is now trying to tax my Chinese income?

Maybe it's time to start looking up which opposition MPs are responsible for these issues.

Definitely it's long since time to get these clowns out of the Beehive and replace them with people who have the imagination to dream up positive, constructive ways to make it actually, genuinely easy for us to pay our loans back rather than just puff their chests out and swagger around menacingly like unusually dimwitted schoolyard bullies.

-

"chris", in reply to

The high life indeed Chris ~ So much for putting your heart into making a genuine contribution to the planet in a manner befitting one’s skill set. So much for choosing a job with little or no environmental impact, a job which not only enables students to immigrate to, do business and study in New Zealand, but also helps to maintain English language’s status as the global Lingua franca.

Googling about the place I slipped on some Whaleoil, (yeah I should have known better) the consensus there being that we are thieves. Theft?

I’m appalled at the amount of IRD student loan advertising on places like Stuff, and the skew the site brings to the party. I have a parents on my case, a well meaning uncle, a fisherman from Kaiapoi, and despite their seemingly genuine concern for my wellbeing there is also that nagging sensation, as you say, that this energy could be put to far greater use were it channeled towards elected representatives. But that narrative just seems to fit so snugly and past realities of free education, a universal allowance, or at the very least not attempting to milk millions in exorbitant interest from progeny’s shriveled udders, seem to have been erased entirely from the collective consciousness of a nation while South Canterbury Finance investors live to fight another day.

It’s not as if New Zealand can’t afford it, I just find it ludicrous, when I left the country I’d made a decision never to return on a permanent basis, of course that meant I’d lose the option of partaking in the NZSF but I can take care of that myself. Now it seems things are more geared to us returning, paying what we can off our loans and in turn qualifying for pensions. Money is clearly not the issue here.

They can call us what they will, and celebrate this system to the ends of the earth but the best thing I feel I ever did for New Zealand was getting off the dole and getting out of the place. That saved the NZ taxpayer at least as much as I owe. But that’s little more than the narrative of a thief.

-

"chris", in reply to

Pretty sure I had to sign something to get a student loan. Marginally sure that something said that it was a loan, and that I had to pay it back

And Keith, beyond financial and legal considerations and your rather glib appraisal of the SL changes, I genuinely value the passion, energy and skill you contribute to the motherland. Great work again with this year's budget.

-

Sacha, in reply to

I slipped on some Whaleoil

apparently the vomit is valuable

-

"chris", in reply to

Now that could be the answer to all my problems Sacha. I could see myself working in whale vomit.

-

Rich of Observationz, in reply to

IRD books things like Working For Families as costs while Treasury carries the interest on NZ's public debt. The actual costs of running the departments are dwarfed by this (in fact, very little of the governments costs are central administration).

-

tussock, in reply to

The whole thing must be quite a lot smaller in reality. People paying a few billion in taxes that they never actually pay and have it show up as both tax and spending in government books is ... weird. Do they even keep track of where their actual tax comes from, rather than just the theoretical stuff?

-

"chris", in reply to

And just to rub a little salt in:The impending Credit Contracts and Consumer Finance Bill:

-

mark taslov, in reply to

STUDENTS LOANED

Having had some time to reflect and do some research I thought I’d come back to this topic:

Pretty sure I had to sign something to get a student loan. Marginally sure that something said that it was a loan, and that I had to pay it back

Most Remarkable for me about this response Keith is that for all intents and purposes you appear to have solved the Global Financial Crisis in one fell swoop, you have at the very least minimized the impact quite substantially, those borrowers should have simply paid back their mortgages, problem solved. Less remarkable is just how widespread this type of opinion with regards to Student Loans is, with this opinion you are most certainly not alone.

While hesitant to make too much of a comparison between Government Student Loan systems and the private "subprime" and adjustable-rate mortgages of the mid naughties, it’s possibly worth noting that while public sentiment largely contends that at least partial fault for the GFC lies with Big Business’s targeting of vulnerable borrowers, this contrasts starkly with the widespread opinion that unmanageable Student Loans are for the most part the fault of borrowers who have, it would seem, targeted our vulnerable Government.

*******************************************************************

Few, if any, would be game enough to dispute that these are ‘loans’, but respective interpretations might diverge when it comes to the expectations of borrowers. Just as you have interpreted:

it was a loan, and that I had to pay it back

Many 1990s borrowers who were fortunate to stumble on the Student Loan stall when cruising the various clubs during O’ week might have just as justifiably interpreted their new contracts to read that they as borrowers will only be required to make installments when earning over the repayment threshold. This was a key selling point for many. Whether borrowers managed to pay all or none of the loan back, StudyLink went to lengths to stress that if the borrowers were earning below this threshold then they were required to repay nothing at that point in time.

you chose to sign those contracts. you did not have to study or you could have found another way to pay for those loans (through a bank maybe).

Oldmoza – stuff.co.nz

So how did these 1990s borrowers qualifyl? Was there a minimum age limit? Were there minimum qualifications? Was a Guarantor required? Tom Oliver was 17 and recently diagnosed with clinical depression when the New Zealand Government lent him his first installment in March 1994, he had qualified for university with the minimum 3 C grades in his bursary exams and despite being underage no guarantor was required to solicit his loan. With a burgeoning drinking and cannabis habit the loan looked like an easy party for an out of control teen. Though he’d ideally still have had a year to complete at school, the 1993 Bursary exams pegged C grades at 49% and the scaling system of the time shifted his 29% calculus up to 49%. While private lenders would most probably steer clear of lending to a student whose qualifying scores (without scaling) were 35%, 29%, 31%, the New Zealand Government at the time was all about giving these kids the opportunity to sign these contracts. To any regretful borrower still lumbered with a loan solicited in that era, a recent headline might be of some comfort:

Editorial: Lower University Entrance pass rate a wake up call for system

Is this indication that recent changes to the qualification system might also entail more responsible lending practices? At the very least it could be taken as indicative of an intent - at least on the part of educators - to limit risk.Tom like many of us ‘qualified’ and voluntarily chose to sign those contracts, but it begs the question; to what extent would these types of lending practices - this bums on seats criteria for qualification - be deemed predatory, and for that matter, one may ask to what extent the Student Loan system, complied or continues to comply with this year’s Responsible Lending Code? That is despite this code being geared primarily towards the private sector. Tom was $7000 in debt to the Government by his 18th birthday and has never been in credit since. Tom’s parents earned $2500 over the Student Allowance threshold and weren’t willing to fund his university education. Despite any bravado, beyond any youthful excess this was not so much money reserved for books or reefers. For the most part the Government offered Tom this 7.2% interest loan so he could stay clothed, fed and housed, while providing allowances to his equally insolvent classmates free of charge and obligation.

-

mark taslov, in reply to

Maybe they had a gun to their head too. If they were happy to take the money, they should be happy to pay it back.

I had my student loan for 20 years - why should anyone who has blatantly avoided making repayments get a free ride?ShaunL – stuff.co.nz

Obviously no one puts a gun to the head of our young borrowers, but just how universally pragmatic are these expectations we have placed on our younger generations? What guarantee does the lender, our Government, offer to assist borrowers in securing incomes above the repayment threshold? Does our country offer jobs or voluntary work opportunities – as is the case in other countries - specifically geared to assist those borrowers who are unable to meet the threshold and make repayments?

The same students and young graduates will hopefully understand economics 101 – a taxpayer funded, interest free handout is simply not affordable.

Elaycee - Kiwiblog

Economics 101 has never been a compulsory prerequisite to soliciting a student loan. Neither is evidence of collateral. You go in with nothing you come out with less + interest. Our Student Loan System, and for that matter most student loan systems hinge on the unfounded assumption that the borrowers will not merely be physically and mentally capable of full time work, but furthermore that they will be financially responsible, endowed with a reasonable portion of common sense and that they will be fully cooperative in meeting their obligations. While for the most part our criticisms of defaulters focus almost exclusively on the latter i.e that defaulters are evading responsibility by choice, and though this convenient scape-goating fits snuggly within the narrative of a Government led by a self-made millionaire, it does largely fly in the face of the reality; New Zealand is a welfare state, where jobs were not available to all, since well before the Loan System was even implemented. The risks the lender faced were self evident from the outset, there were bound to be losers, this is fundamental to the nature of capitalism.

Certainly there were those under 25s who managed to secure allowances by entering into marriages of convenience, but has anyone in the Student Loan System ever enjoyed a truly free ride? Yes foreign nationals need only qualify as permanent residents and be in the country for 3 years in order to qualify for a student loan which they could quite easily later evade the repayment of by returning home, but even so, would this qualify as a free ride? Three years in New Zealand is the price paid.

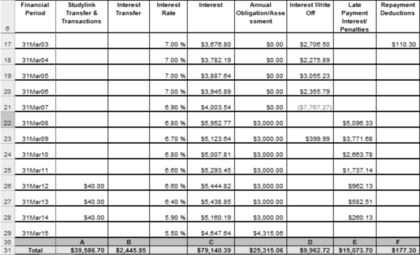

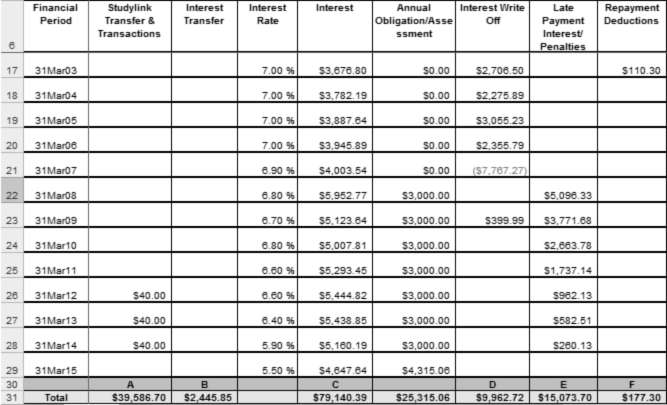

In March 1993 Susan Isherwood received her first installment of a loan that would reach $50,000 by her graduation in 1998, In the years she’d been studying the loan had accrued interest of 8.2% in 1993, 7.2% in '94, 7% in '95, 9% in '96, 8.4% in '97 and 8.2% in '98. Desperate to repay this and unable to find appropriate full time work in New Zealand in order to make a dent in that loan while based here, she went overseas in 2001. Interest on Susan’s student loan was 8% in 1999, 7% from 2000-06, 6.9% in '07, 6.8% in '08, 6.7% in '09, 6.8% in '10, 6.6% 2011-12, 6.4% in '13, 5.9% in '14, 5.5% this year. As of 2015, when adjusting for inflation, and without adding the interest following graduation, Susan’s Student Loan would be about $70,000. As things are with interest and penalties, Susan currently owes the IRD $160,000.

Back in ’99 I phoned IRD to tell them I’d be going to China and to explain that I’d be earning the then equivalent of about NZ$500/month and I couldn’t see how I’d be able to make the minimum repayments. I was told, tough, you have to pay anyway. About 6 months later a friend got a job on the outskirts of Shanghai earning about the same. She’d phoned IRD and had been told she could apply for some financial hardship thing and get off the compulsory repayments.

This caught my eye Chris because although it’s quite likely that I am mistaken, as far as I can see looking over various student loan statements there were no penalties in ’99. As far as my own student loan statement shows there was no Annual Obligation/ Assessment until March 2008 and likewise no Late Payment Interest/ Penalties until the same date – introduced following the ‘Amnesty’ near the tail end of the Labour Government’s final term, I assume.

In late 2013, overseas “defaulter” Stu Jack, perplexed by the threat of arrest, made a Financial Hardship application. Living in a developing country, earning the

average wage there of about $5000 p/a - equal to the annual $5000 repayment requirement on his loan - he was unable to afford to meet his repayment obligations, and thus accruing penalties in addition to interest. Based on his circumstances he assumed his hardship application would be successful, this would have entailed these penalties and his outstanding overdue obligations being wiped.Unfortunately Stu had for two years been married to a local who, prior to their relationship, had quite understandably accrued life savings in order to cope with the lack of welfare system, lack of free healthcare and lack of superannuation in her country of birth. Though alarm bells rang when Stu first read through the application noting that it also requested that he provide financial records for his wife in addition to his own, staff at the IRD reassured him that his spouse’s finances would not be taken into consideration except to calculate total household costs.

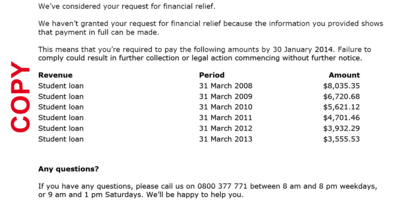

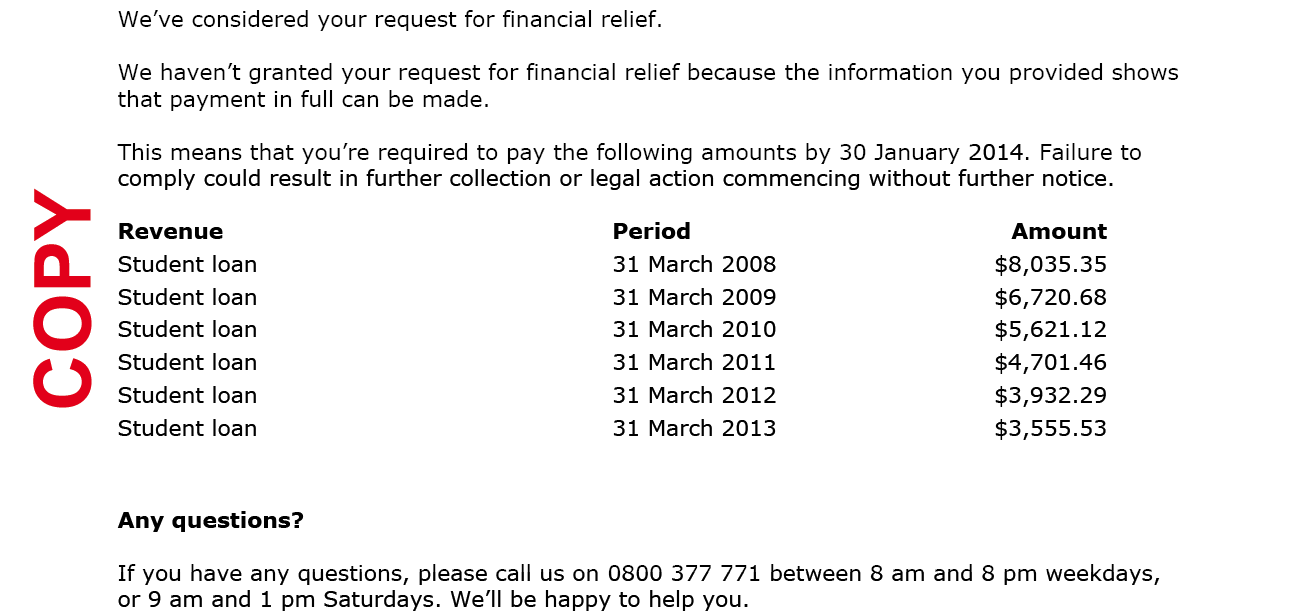

A month later Stu was forwarded a PDF notifying him that not only had his hardship application been declined but that as he had failed to meet his obligations, he was required to pay roughly $36,000 without further notice or face legal action or collection.

He was not being penalised for his own earnings but the savings of his spouse. The savings of a foreigner earmarked for – what few may deem – superfluities; such as admission to hospital in a country with a prepay health system and the convenience of keeping that IV connected after the fact. Stu was penalized for marrying a local with good fortune enough to have a safety net in place, or more to the point, Stu’s spouse - who all things considered the money actually belonged to – was being penalized for marrying a New Zealander with an outstanding student loan.

Essentially, New Zealand Student Loan borrowers are being threatened with legal action from the IRD unless foreign spouses repay the IRD. As a worst case, foreign spouses are possibly also threatening divorce from New Zealanders rather than fork over foreign savings to the New Zealand Government. Money that could pay for vital medical care in countries where none is freely provided is being targeted for repossession by the IRD in order to repay NZ Student loans. As a nation have jumped to shark. The borrower, faced with the prospect of returning home and still being unable to pay off the loan and in turn being arrested at the border if ever trying to leave the country again would obviously be in a quite the fix.

-

mark taslov, in reply to

Which are all beautifully miserable sob stories in their way. We hear the entitlement of exiled ‘90s borrowers and we notice the dearth of 30-40 year olds in our society. We could, as Toby Manhire suggested, prioritise the immigration of more refugees to New Zealand, to take up the slack, like a revolving door. But what of this missing generation, the 30,000+ student loan defaulters? The prospect of returning with any of this overdue entails threat of arrest, court action, collection and then the privilege – as Susan pointed out – of competing with Australians – to whom our Government dole out interest free student loans without their having to endure a day in the compulsory education sector. We do have enough well educated people, they’re just not all here, and we’re offering very little in the way of incentive for them to return, while offering considerably better to those brought in to replace them. Factor in the other 970,000 New Zealanders living overseas and it becomes quite clear that money is not the issue here, neither is attracting people. The issue is – or at least until very recently was – retaining our population.

30,000+ people? What is that? That’s more than a full Nelson, that’s a Whanganui back in the day, and while New Zealand was twittering away about whether to include an ‘h’, a population roughly that size chose to ‘flee’ New Zealand with the money and the bag. Flee with their millions, buy a mansion in Brazil, puffing Cubanas, set for life – is how some would portray it; A conspiracy of the ‘90s crew, despite only 4413 borrowers having debt of more than $100,000, including 967 who owe more than $139,999. So what prompts a small New Zealand city to defect with insufficient funds? Are these 30,000+ idiots? 30,000+ ungrateful wretches? 30,000+ New Zealanders whose only dream in life was screwing New Zealand out of a few thousand dollars before scooting off to Nirvana? What is actually going on in our compulsory education to produce 30,000+ New Zealanders – who for want of a better term – would do over our country? Loosely, that’s exactly the borrowers’ objective, at least that’s how it appears to have been portrayed by Government Ministers over successive administrations.

Is there a possibility that this exodus was not motivated solely by greed? Perhaps it could have been prompted not so much by a glut of something negative but more by a lack of something positive, for example; opportunity. Could lack of opportunity be the reason at least some borrowers left? Has lack of opportunity ever been an issue? Was sufficient opportunity available to graduates through the 1990s? To what extent did opportunity feature in the economic model and policy implemented? And not to overstate things, because there were opportunities around: Tom Oliver had the option of working in a cannery full time only to turn it down. An Art Literature major with an IQ of 143 could have made good in the cannery, working his way up to cannery manager and repaying his student loan within twenty solid years, ample time to prepare for a life after his financial graduation. Unfortunately, following his academic graduation Tom felt he was better than all that, and no doubt the Art Literature Department played its own role to in heightening his ambition – he like so many others fled, to opportunity.

Buddy, if you stay and work in NZ like some people chose to do you do pay “something”. The whole point is that no one is chasing the loan doddgers overseas but sticking it to people who have been honest, paid and stayed in NZ to work for shit pay and try and pull this country out of the hole it is headed into.

Immigrant – kiwiblog

Many of those who stayed have been empowered by their student loan experience, it has provided a sense that we have contributed, but in some cases this has also led to a derisive attitude to those who haven’t, to those who have for whatever reason been unable to. While not an unusual outcome given the nature of our education and socialisation: “I put up the tent, I lit the fire and I raised the flag and you did nothing! Nothing!” it does rather miss the point that to some extent the New Zealand based borrower was in part afforded the opportunity by the absence of the overseas defaulter. Subtract 30,000 people from a workforce the size of New Zealand and you’re bound have more chance of nabbing that job, these defaulters are similarly skilled, it was in acquiring these similar skills that they amassed these loans.

Of more than 700,000 borrowers, about 101,000 live overseas. Overseas borrowers owe about $2.67b, of which $411.5m is overdue. Bear in mind that it is common for debts to be http://www.studentloan.org.nz/blog :400% – 800% higher than the actual amount borrowed, a far cry from any inflationary accumulation. All up about 1,000,000 New Zealanders live overseas. That’s not just a statistic, that’s a phenomenon, that’s the population of Auckland circa ‘82 give or take. Are any of them employers? Could they be pursuing the same opportunities in New Zealand? Could they be providing the same opportunities in New Zealand? At what point does Government interest and action in this economic area, specifically the area of creating opportunity, become a priority? When does this lack of provision in the way of policies gear to providing greater opportunity, for all New Zealanders – not just for those of us employed at Fonterra – tip the scales and start to become a significant impediment to getting ahead – not just to those who would choose to leave but to those who would – if they could – return here?

$800,000 salaries for top city staff the market rate, says mayor

When did taking a $400,000 paycut and providing 8 more jobs stop sounding like a good idea? When did “Good for the economy” become synonymous with ”Good for the people”, and how is that working out? These two things are quite definitely not the same, one need only open one’s eyes a couple of degrees to see that this machine is in dire need of an overhaul. The empty store fronts along the main streets of Hastings, Wairoa, Waipukurau tell us this. The youths gathered outside the Pack n’ Save sifting smokes, the fried out Herbal High vagrants wandering glassy eyed, uttering obscenities, are all in their way by products, traceable back to actual policy. This is not a success story.

When did becoming a councilor, generally speaking, cease to be primarily about being a stand up citizen and become more of a career? Could it have been around the same time we collectively decided that athlete or media personality were desirable qualifications for managing our communities, most probably also around the same time the cost of photocopying and stapling a LIM together breached the $100 barrier. We, our country, are not providing enough real opportunities for real people, and this has been the case for quite some time. Was 30,000+ overseas defaulters part of the game plan or were our policy makers taken unawares? Has a New Zealand Government willfully implemented a polilcy entailing the prospect of issuing 30,000 arrest warrants, funding 30,000 court dates? Did voters vocally express a pressing need for less police officers keeping the roads safe and a dramatic increase in Government legal costs? What has happened to the governance of our country in the mean time?

-

mark taslov, in reply to

Oh – and I forgot to add: Student debt is $12 Billion, with a bad-debt write-off of approximately 45%, so the taxypayer will have to find 5.4 Billion of this. Plust we are paying approx half a billionin interest.

So not only did I pay interest on my student loan, I’m now having to pay the interest on all the other fucking ingrates.Spam – kiwiblog

The invective permeates. As if this were real capital that could have bought Spam an actual house; real money rather than numbers on a ledger of a lender who can never be bought out despite doing its darnedest to sell itself off. It’s like a game of ‘Simon Says’, were Simon called Bill:

It’s a little horrifying in terms of its aggressiveness, but I also think it makes sense in a lot of ways. Aside from raising the amount of money which is collected, it’ll also make it less attractive to try to flee your student loan debt, or to get into the situation where interest stacks up to the point where it becomes impossible for graduates to move back.

It’s a big, hideous stick, but I guess good policy doesn’t have to be all carrots.

But it may not be good policy, it may be ridiculous policy, it may even be preposterous. The carrot is and always has been interest free loans for borrowers who remain in New Zealand, assuming we can all agree that the object is to recoup funds, a stick designed to make return impossible for graduates whose interest has already stacked up doesn’t sound quite fit for purpose. Interest free loans for borrowers who remain New Zealand based has already been immeasurably attractive for quite some time. Stay in New Zealand and accrue no interest, go and the loan grows with you. If you’ve been working legitimately in New Zealand from the get-go you’re not overdue, if you’ve been working under the table – quite common place as anyone eavesdropping in provincial bars will confirm – from the get-go, you’ve officially been earning nothing and you’re not overdue. You can leave with no fear of arrest. If you move overseas and the interest stacks up, well that’s always been the case, nothing in this policy amends that situation. Coming and going might become a bit of a problem, but for anyone who is dead set on making off with the dough following graduation the package tour remains; Default or Bust. When based overseas the interest grows as it always has, but yes, under certain conditions it may seem or feel impossible for graduates to move back.

So what now qualifies as “good policy” in New Zealand is at least in part; making it ‘impossible’ for graduates who’ve stacked up to much interest to move back to New Zealand? We know without a doubt that there is nothing in the policy preventing defaulters from actually returning to New Zealand so the question to the voter is; does this sound like a winner? How much money is making it impossible for New Zealanders to return to New Zealand expected to recoup from those New Zealanders? Quite reasonably one might be given to assume that ideally at some point, recouping the money would be the goal of the exercise, hence the interest and the incurred sleepless nights. Bear in mind that I’m not asking if the IRD should be threatening litigation or collection against those with sufficient funds flagrantly shirking their responsibility, what I am asking is whether implementing a policy to arrest, to detain and to split up the families of those borrowers – those with absolutely nothing to show for themselves – is quite as credible as solution to recouping investment as the nodders and yes men would have us believe.

By October 2014 more than $6 million of student-loan debt belonging to 99 overseas-based Kiwis had been written off in that year – an average of $60,000 each. The number of overseas-based bankrupts having their loans written off more than doubled from 42 in 2013 and from 35 to 45 in 2010-12. It almost looks like we’re creating a new industry, but this is not the type of opportunity to which I refer.

So what of Susan and her $160,000 loan? Prior to attempting to venture home in 2014, as one of the 30,000 defaulters Susan applied for a hardship application and was successful. This not only meant her penalties were wiped, but also that any overdue amounts were cancelled. Satisfied with this result Susan arrived home for Christmas facing no prospect of arrest for lack of payments. While in New Zealand she made no attempt to repay any of her loan, the amount now abstracted beyond the realms of tangibility – equal to 14 annual salaries. Any repayment she could have afforded would have been swallowed up by the subsequent year’s interest and without ever having been employed or having any real prospect of pursuing her vocation in New Zealand, Susan rightly or wrongly earmarked these earnings for her own superannuation in her adopted country.

In contrast, Tom, also based overseas, earns well above the threshold and by paying bits and pieces over the years he’s managed to maintain his outstanding balance at roughly the amount he borrowed. With no family based in New Zealand he has no plans to return home and he remains adamant that the implementation of this new policy means absolutely nothing whatsoever to him. Tom clarifies that he would be more than happy to settle back in New Zealand if it provided the same opportunities as his adopted country. Certainly the prospect of arrest/ legal action on return is not as oppressive a stick as it is being bandied about to be. If per chance Tom were to visit New Zealand and then be arrested he seems quite confident that paying off the $2000 court fine and the overdue amount would still be in no way conducive to his deciding to pay back any of the loan proper, and given the size of Tom’s original loan and what it paid for – for the most part basic sustenance – this outlook is not entirely incomprehensible.

As for Stu, on his third attempt filing a hardship application he managed to convince IRD staff that it wasn’t in the NZ’s best interests to be threatening legal action against him for the savings of citizen of a developing country with a pre-pay health system. He is now free to come and go from New Zealand for the next 8 months, that is at least without the threat of arrest for his loan. However with a shortage of pocket money for any imminent visit the loan balance continues to grow and he is now looking seriously into the prospect of declaring bankruptcy. Again, the key reason cited for not returning home is the lack of opportunity within his field of work. Stu could possibly be regarded as the greatest success of this policy in terms of achieving the interpreted objective of making it impossible for borrowers to return home.

Happy to report that I had a student loan during the nineties and paid off, even paid interest, all with a young family on tow.

No complaints from me

But will easliy complain about those who believe they had some form of entitlement to this priviledge. I agree on the previous poster that Graduates shouldnt leave these shores on a working holiday unless they have paid their debt to the taxpayers, its the least they could do to show thanks to the NZ Taxpayer, not only for funding 70% of their course but who have lent them the money to do so.Rat – Kiwiblog

Rat is not entirely wrong, while he successfully paid off his loan without any semblance of the limitations he would impose on new borrowers, his suggestions offer more in the way of discussion than a hundred other commentators whose key contribution is “I paid my loan and everyone else should too, because I could.”. These other contributors, while often impassioned, don’t so much offer solutions as much as they offer an attitude, a widespread attitude, a morally defensible attitude, a dismissive attitude, but no solution to recoup a cent. For those who can afford it there’s nothing to fear, for those who can’t: they have nothing to offer regardless. Factor in policing, legal and court costs and this policy has the makings of a very expensive exercise for very little guaranteed benefit whatsoever.

Susan likewise has suggestions; that all interest be wiped and that historic loans be recalculated to match inflation. Tom, while less forthcoming, feels that it is wrong for New Zealand to be forcing under 18s to take out loans to pay for living costs, and when pressed he feels that a universal allowance would level the playing field considerably. Given the applications are only retrospective Stu is already resigned to filing for hardship annually and would be glad enough if the IRD could conclusively stop threatening legal against his wife’s savings, ideally he’d like to believe that New Zealand could make a concerted attempt to consider something akin to Peru’s intention to introduce free higher education by 2016 though he remains realistic that matching Peru may be a little beyond the scope of a country like New Zealand under our current Government .

-

mark taslov, in reply to

Stu has already dealt with 20+ staff members at the IRD Overseas borrowers Department, he is more than familiar with the fact that the system has been designed in such a way that rather than there being some superior qualified to make the ultimate decision as to future applications, his application will be subjectively handled by whoever picks up the email, his enquiries will be handled by whoever picks up the phone and therefore given his past success rates in filing these applications there can be no guarantee of future success regardless of the stability of his situation. What remains consistent is that any married applicant filing for Hardship dispensation is required to include as much financial information for their spouse as for themselves, and this is why I make no bones about calling out this policy for the dog it is.

It would cost $600,000 for Inland Revenue to set up the border arrest system for student loans, and those prosecuted in court could face a fine of up to $2000.

Stephen Joyce

As any defaulter should now be aware, returning home may now result in arrest when attempting to later leave New Zealand. For a borrower like Tom this represents a departure tax, if per chance he manages to enter and exit New Zealand without paying a cent well then he’ll know well before the rest of us that this policy is more of a limp chamois, sponging that grill, than anything objectively stick-like. This would not be such an unlikely conclusion to reach - as may already be inferred from the apparent ease at which borrower and convicted murderer Phillip Smith was able to flee - any current enforcement of this policy is troubled at best.

For Susan or Stu; being arrested and fined represents something quite altogether different. As they continually fail to meet their obligations and if they fail to successfully apply for hardship status then the prospect of arrest, court and fines looms over any planned visits. Given they both have family here, and given the fact that their annual obligations or even just the interest is already well beyond the price of an airfare home, this would not seem an improbable scenario. This is where - as some see it - the policy hits a bump. What happens once that fine has been paid? Their annual obligations and even just the interest are often far in excess of these fines.

There is a saying "don't make threats if you're not prepared to back them up". These threats may garner some success in recouping funds, this recoupment may be significant, but when it comes to Government policy, ideally all factors, the effects on all people, will be considered, and when it comes to Government policy in the long term; “pretty legal” probably won’t cut it. So what happens to Stu if this threat is followed to the letter and he is arrested and ordered to pay a fine which he can’t afford and tries to leave the country again? Will we arrest Stu once more and pay for a second court date - issue a second fine? There is absolutely no question that Stu would want to get back to his wife and family and you’ll no doubt notice the likelihood of a cycle emerging in the eventuality of us arresting an individual thus incline, a possible eventuality whereby NZ ends up forking out significant legal costs for no recoupment whatsoever.

Critic would have us believe that inevitable outcome of this type of cycle would be prison time. If as would be the case; Stu were to be imprisoned for lack of funds, for failing to file his hardship application or for having a spouse with savings or an income over the threshold then we’ve already found ourselves with further unanswerable questions. In the current environment many may be satisfied with Stu’s imprisonment, some may be happy, some may even –for want of a better term – class this policy as “good”: Imprisoning Stu, not because he ever earned over the threshold but because his wife has. What would be the ramifications of such an action moving forward? Were Stu’s wife to divorce him then the funds the IRD has prosecuted him for withholding are no longer a part of the equation, would he then be free to go?

More to the point; countless defaulters do recall, with absolute certainty, that something said you only have to pay back when earning over the threshold, that was in the contract, there was no mention of punitive measures for marrying a well endowed spouse and failing to secure said spouse’s funds for the purposes of loan repayment, that didn’t feature in the contracts the large bulk of us signed. And yet, now there is the very real practice and prospect; the spouse’s funds are playing the key role in not simply ascertaining whether a borrower can make repayments but also in whether the New Zealand justice system can and should arrest, prosecute, fine and quite possibly imprison New Zealanders, New Zealanders whose crimes entail not earning enough money and marrying someone with too much.

Anyone who’s been on the bad end of a divorce can tell you how many ways this type of policy can go wrong, and all it’s going to take is one stubborn nut to crack that policy wide open like a fresh egg on an early Tuesday morning. This is no longer about the borrowers, the defaulters, this is about their families and the myriad possibilities and positions such relationships encompass. We are already well beyond New Zealanders, citizens, residents and those who qualified for a loan. Despite being in possession of full and frank documentation that borrowers are earning well below published income thresholds the IRD has now shifted its focus to spousal assets with absolutely no attempt being made to verify whether these assets are indeed legally speaking - relationship property. This has become about testing the parameters of ongoing relationships. How much should a New Zealand borrower who is the forth wife of a Shia Saudi Arabian be expected to extract from her husband? And why have we established a policy to arrest her if she fails? That’s not a decision she is necessarily legally qualified to make. The decision to pay these sums that are being recalled by the IRD at the threat of arrest now lies in the hands of foreign citizens, citizens who are far beyond the IRD and our own Government’s jurisdiction. The IRD and the Government are ethically so far out of their depth with this policy that it feels almost callous pointing out the gaps, but given the lack of careful attention the media has given this issue, and knowing enough about this - in the interests of transparency - I feel that it is high time someone put it all down here. It angers.

-

About $7 million has been spent on a tracing system by which Inland Revenue is working with debt collectors in Australia and Britain to find borrowers and get them before the courts, some will keenly attribute success specifically to this policy,

"This is working really well, particularly in Australia, where there are 10,000 borrowers, many of which can afford to make payments but aren't," Mr Joyce said.

"These initiatives have a running return where, every $1 we spend, $11 is collected back."That leaves us with 30,000 overseas defaulters minus up to 10,000, free to roam without threat of apprehension at their respective borders if they choose to jump ship from one adopted country to another. That is if they choose to continue to aggressively evade the system, which would largely depend on whether they decide that New Zealand still doesn’t offer sufficient opportunities to inspire a return home. If they refuse to return - that they refuse to return - can in itself be cited as ample evidence that we, our country, our systems, our economic policies, our cultural systems are tangibly inferior to those on offer. 30,000 people can be wrong, but only if a system’s flaws grant them license to be. Until we are capable of acknowledging that this system might be fundamentally flawed, at least in terms of the manner in which it’s currently being administered, then our progress as a society will be negligible. but in order to develop, we firstly need to check our attitudes, expectations and ideals, because “Marginally sure that something said that it was a loan, and that I had to pay it back” recoups nothing, pointing fingers, vindictive epithets and talking ourselves up simply won’t pay off this debt, this is an issue of perspective - like or perhaps unlike a PM’s hat - without wearing this thing we have very little in the way of traction to even consider attempting to fix it and we will continue to watch this debt balloon, grinding our teeth. It’s time we reexamined our legacy.

It’s not so much that we want opportunity or even for that matter that we demand opportunity: it’s that all things considered we as a people deserve opportunity. Not just in Auckland, Christchurch or Wellington but throughout the country, and now far beyond. Empty threats may not be the best substitute, opportunity rather than sticks, good policy not bad, these might bring our boys and girls, sons and daughters, cousins, uncles, aunts and even parents back home, perhaps not. But as should now be evidently apparent, to all but the most enthusiastic conspiracy theorist, waving that stick – no matter how hard – won’t turn Jack’s magic beans to coin.

*Names have been changed to protect identities, naturally.

-

ETA: the 30,000+ defaulters figure quoted above now appears to be well shy of the mark:

There were just under 109,500 overseas-based people with student debt at the end of June last year, and they were a collective $863.3million behind in their repayments, with over 70,000 of them not meeting their repayment obligations.

-

A Kiwi living overseas who refused to repay his student loan has been arrested at the New Zealand border.

This is the first time the sanction has been used. The man was detained on Monday while trying to leave the country, Inland Revenue confirmed.

He has lived overseas since 2004 and has a student debt of more than $20,000, the New Zealand Herald reported.

-

izogi, in reply to

Radio NZ has had some significant coverage in its 11am news bulletin, but with nothing significant online just yet that I can find. [Edit: the online version has just been updated.]

The 40 year old man is apparently claiming that his loan was about $40,000 when he left New Zealand, but has since blown out to around $130,000 due to interest.

-

chris, in reply to

$40,000 when he left New Zealand, but has since blown out to around $130,000 due to interest.

Thanks Izogi, quite possibly not an altogether unusual scenario

As at April 30, 2013, there are more than 2,200 overseas-based student loan borrowers whose loan balances are over $100,000..

From your link:

He has been allowed to return home after his family paid $5000 to Inland Revenue – they also had to provide another $2000 to his lawyer.

Boom times loom for the legal profession. Not so boomy for families of defaulters.

-

chris, in reply to

ETA

It turns out that the arrested defaulter is the Cook Island Prime Minister’s nephew.

Steven Joyce:

"Our preference is that people just meet their obligations and that’s the important thing because you can’t forget that these people have had the benefit of loans from the tax payers to be educated.

Giving credit to The Honourable Mr Joyce he is absolutely right, without these loans, the greatest proportion of which is allocated for living costs for the majority of courses, many students wouldn’t have the benefits of accommodation, electricity and food while studying.

-

Moz, in reply to

many students wouldn’t have the benefits of accommodation, electricity and food while studying.

And of course, if they weren't studying they wouldn't have those expenses.

You could argue that we should pay all students, even foreign students, enough to live on while they study, but I don't think that's this discussion. This one is all about the miracle of compound interest.

-

chris, in reply to

This one is all about the miracle of compound interest.

This is a

Post your response…

This topic is closed.