There's some pretty heated debate over at No Right Turn and Kiwiblog about the nature of KiwiSaver, and unfortunately, I think both DPF and I/S are very far off the mark.

It's taken the weekend to sink in, but the simple and obvious truth is that the government can't make your pay packet magically increase by 4%. Cullen has mentioned the "downward pressure on wages" that the compulsory employer contributions will have, but little has been made of how much of a downer this really is. The scheme is still as sensible as it was last week, it's just lost most of its "woohoo - free money" charm.

It will certainly push wages down.

Employers are going to take KiwiSaver contributions into account when setting wages and in considering wage increases. The compulsory contributions will be absorbed into wage levels in the medium-term (~3-5 years). However, it's not going to be the full 4%, because there's also the tax credit to consider.

Wages are still going to increase, but just at a slower rate until the changes are absorbed. Once they are, they will have no effect on wage levels (unless the compulsory contribution levels or tax credits are adjusted).

Your real wage (your nominal wage + what you get back from your employer via KiwiSaver) will be unaffected.

It won't hit the poor.

Employers are only justified in pushing down wages in proportion to the amount they pay into KiwiSaver, minus the tax credit that they receive. It means that low-income earners will be less affected by the downward pressure on wages.

For example, for a worker who earns $30,000 p.a. and puts $1,200 into KiwiSaver, an employer is only going to have to match $108/year - the rest is covered by the government. The downward pressure on wages is directly related to the cost to employers, therefore, the impact on low-income earners is minimal.

(For someone on $60,000 p.a., the employer will have to pay $915. See spreadsheet, under "Employer Contribution (Net)" for more details.)

The rich will benefit more, but not the way you'd expect.

As the first part addresses, the dirty little secret behind KiwiSaver is that the employer contribution is an illusion. The government is making the employer make you pay. And the government contribution is capped (with an exception that I'll explain) at $2080 per year. What this means is that as the personal contribution increases, the employer contribution also increases - but this is meaningless, as the employer has already recovered this amount through reducing your wages! The government contribution stays fixed and all the increase is - directly or through your employer - coming from you. Ha, you've just been tricked into saving for your retirement with your own money, sucker!

What this means is that the extra employer contribution is not really a "benefit". It's just your own contribution, slightly recycled.

But ah - KiwiSaver has *another* dirty little secret. By making part of your wage go to your employer as a compulsory contribution, it never becomes part of your pay packet, and so you don't get taxed on it. It's practically a tax cut. This is the only income-dependent part of the government contribution - i.e. The bigger your pay packet, the more you get. So if you include the portion they don't have to pay in taxes, then it does benefit the rich, but it's not huge, either.

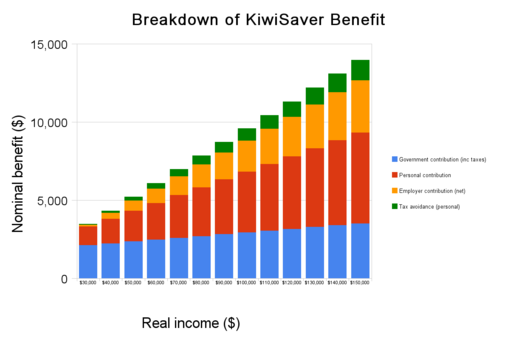

Here's a graph. Click on it to see a bigger version.

Note that the personal contribution is the biggest, but the employer contribution is actually very small do begin with, as most of the personal contribution is off-set by the government contribution. This grows pretty slowly (the bit that increases is the superannuation tax exemption that businesses get, which the government counts as part of their contribution), while the tax avoided grows. And yes, it gets bigger as you go up in income.

(Apologies for using a bar graph. Google Spreadsheet can't do area graphs, and I can't figure out how to make OpenOffice spit graphs out as JPEGs. Google sure makes them look pretty, though. Okay, maybe not so pretty when they're scaled down. Hideous, in fact.)

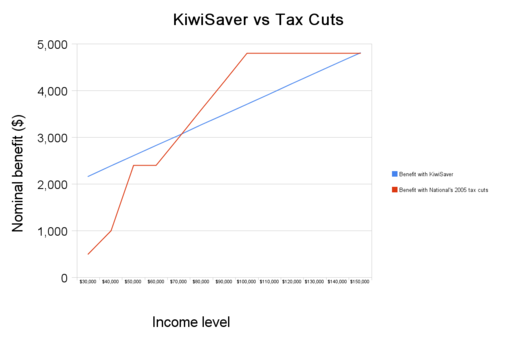

Where both DPF and I/S got it wrong is that they treat employer contributions as if it would have no impact on wage levels - i.e. That employer would just agree to pay this extra 4% out of their own pockets forever. They won't. And so, it won't have either the redistributive effects that I/S hopes for, nor the outrageous benefits that DPF implies. Instead, the employer contributions need to be written out of the equation - it's a fiscally neutral part of the scheme aimed at changing behaviours (i.e. Holding your money to ransom so you'll save). The only real place where the government is pumping in money is for tax credits, as well as the tax avoidance mentioned above. With these in place, how does it compare? Here's one I prepared earlier.

Those on $30,000 p.a. benefit the most from the $2080 tax credit for KiwiSaver. Since the $2080 tax credit is capped and the tax benefits on the savings is small, it gets overtaken by tax cuts around the $70,000 p.a. mark. But the tax cuts are to the thresholds, not the rates, which effectively caps them at $4,800, so at $150,000 p.a. Income KiwiSaver takes off again. But keep in mind that they're still only getting $2080 from the government, they're only benefiting because they're not paying tax on the employer half of their savings.

Not that a direct comparison of the two has any validity, unless National provides an updated costing, and then you have to consider inflation, inflation, interest rates, exchange rates and inflation. But there you go. If you want to compare the two, head-to-head, without comparable costings, and then ignore the macroeconomic consequences and focus exclusively on nominal return, then here you go.